“You should only invest in Bitcoin what you can afford to lose”, said Jon Matonis, executive director of the Bitcoin Foundation. Unfortunately, not everyone will follow this advice. While a few have become millionaires in the crypto-currency space, many more have gone into debt, or lost money, while trying to create a sound retirement. For those with retirement funds they simply cannot afford to lose, we must move to the other end of the investment spectrum, and look at what has worked for thousands of years. There is plenty of ground to cover in between these two extremes, and we will touch on several of these options as well. Please keep in mind that individual circumstances vary, and this article does not constitute investment or tax advice. It is intended to serve as an educational or informational resource, to help you make wise financial decisions on behalf of you and your family.

Alternatives for Retirement Income

People are looking for alternatives when it comes to finding retirement income, and for good reason. Nearly 90% of the working population used to be covered by pensions. That number has dropped to about 30% today, according to the National Public Pension Coalition. While pensions for many are nonexistent, those that have pensions often cannot count on them lasting throughout retirement. With budgetary and debt problems, many state-funded pensions are facing setbacks and adjustments lower. In the state of Illinois, the level of desperation has led the legislature to float a plan to borrow over $100 Billion at 6%, to invest in the stock market - hoping to achieve gains to help shore up their bankrupt pension systems. It is not only governments having trouble paying pensioners; many union and pensions have been slashed as well.

Foreseeing the difficulties of paying lifetime pensions to retirees with an expanding lifespan, corporations began exchanging pensions for asset-based contribution plans, such as the 401(k) that many people have today. What makes the retirement plans of today different from the pensions of yesteryear, is portability, and personal responsibility. The employer used to be mandated to manage company retirement assets in such a way to provide a lifetime of income to employees dedicating 20-30 years of service to the company. Today, employees can leave an employer in 3-5 years, and take their retirement savings with them. However, the investment results, and the income produced by those assets, are largely the responsibility of the individual. Most 401(k) plans, sooner or later, are rolled into an IRA account. The choice of where to place these IRA funds becomes of primary importance, as it has the potential to impact retirees (and their families) for the rest of their lives.

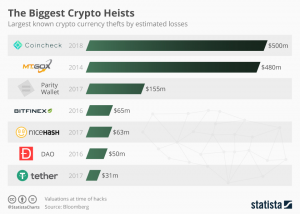

While crypto-currencies might be an exciting place to speculate with funds you can afford to lose, it does not seem to be a safe place for retirement funds you are depending on. Since 2014, over $1.3 Billion in crypto-currency has been stolen. That is only what has been reported. $500 Million was stolen as recently as last week (1/26/18). There are also those that still have their cryptos intact, but worth 50% less than when they purchased them a couple months ago. There are also scandals and computer viruses involved with mining these currencies, that corporations and governments are clamping down on. In many ways, the Crypto arena seems like the Wild West, and perhaps not worthy of your serious money at this time.

Deciding where to invest Your IRA

Deciding where to invest your IRA can seem like a daunting task, for those not trained to manage money. There seems to be an ever-expanding list of opportunities, which we will discuss in turn. There is much talk today about investment-related expenses, and the admonition to keep them low. While expenses are certainly one point to consider, it is also important to remember the old English adage about being “penny wise, but pound foolish”. Simply put, it is more important to have your retirement funds held in the right places, than it is to pay the lowest fees. The most important factor to consider is obtaining a good value. Warren Buffet famously explained that “Cost is what you pay. Value is what you receive.” It is better to preserve your retirement funds by investing in a proven strategy with reasonable fees, than to lose or shorten your retirement by paying lower fees for a losing strategy. Costs are only as important as the value received.

The proliferation of low-cost investment options has been promoted with the mantra that “fees matter; a small fee can add up over time...”. While this might be true if individual investment habits were always beneficial, most often the low costs of low-service investments are outweighed by the lagging performance that results. Left to themselves, people often do the wrong thing when it comes to managing their investments in the stock market. https://seekingalpha.com/article/4108688-investor-returns-vs-market-returns-failure-endures While some tout the oft-repeated idea that “...the stock market averages 10%...”, the reality is that most people in the stock market earn much less, on average. During a recent 30-yr period for example, while the S&P 500 Index averaged over 10% per year, the average stock market investor (including those invested in “low cost” index funds) averaged less than 4% per year, over the same time period. Bond market investors fared little better, averaging 0.4%, when the underlying bonds averaged 3.97%. We do not believe that bank accounts are worth considering for retirement funds, with some charging more in fees than they pay in interest.

Of course, these returns do not take into consideration the effects of inflation, or what happens when the Dollar decreases in value over time. When adjusting for these realities, gold and silver really begin to shine brighter than other alternatives. It turns out that precious metals often beat the stock and bond markets, when it comes to protecting purchasing power in retirement. We explained this dynamic a couple of months ago here. It is really not hard for individual investors to do, when working with seasoned professionals at the US Gold Bureau. They have helped thousands of Americans secure their retirement, and would be glad to help you as well. Here is a link to some information, to help you get started. They can help simplify the entire process, and help ensure your financial future.

Retirement Income

Replacing income in retirement is difficult to do, and the placement of your retirement funds should be done thoughtfully and with care. It should be put in something that will last. As described in the best-selling book “The 7.0% Solution”, gold and silver are described as “Forever Money." In the same way that a “forever stamp” purchased years ago will still deliver the letter after postage has increased in cost, so gold and silver will help preserve your purchasing powers in the days and years ahead. An ounce of silver will purchase as much grain today, as it would in 300 BC. Minimum wage in 1964 ($1.25), paid in silver quarters, equals $19 today. 100 ounces of gold in 1970 ($3,800) would buy a new car then. The cash $3,800 today, would not buy a good used car. But the same 100 ounces of gold today ($135,000), would buy 2 new luxury cars. In retirement, as in life, the cost of goods tends to go up when priced in paper money. We think it makes sense, that some of your retirement funds should be invested in something with a proven ability to keep pace. Something like gold or silver...

Get Our Free

IRA/401(k)

Investor's Guide

Posting in: